Summit Business - Reaching the Top

Summit Business - Reaching the Top

Finance, in simplest terms, may be described as the discipline of managing, allocating and investing surplus money in a value-maximizing manner with minimal risk to contribute to the country's socio-economic development. The composite financial sector includes corporate finance, investment analysis, behavioral finance, financial markets and institutions, risk management, international finance, and public finance. These expertise areas can allow organizations to perform well in capital structure, dividend policies, and governance; aligning the risk and return relationship; and analyzing asset pricing models. With the help of behavioral finance, the direct impact of certain psychological biases on the financial decision-making process is investigated, and the financial markets provide impetus to fund transfers and asset pricing. Risk management assists the organizations in identifying, estimating, and controlling different financial risks while international finance explores the effects financial systems around the world have to the different economies, and public finance looks into the government's utilization of public money through the exercise of taxation and the effect it has on the national economy.

Topic Focus: Capital structure, dividend policy, and corporate governance.

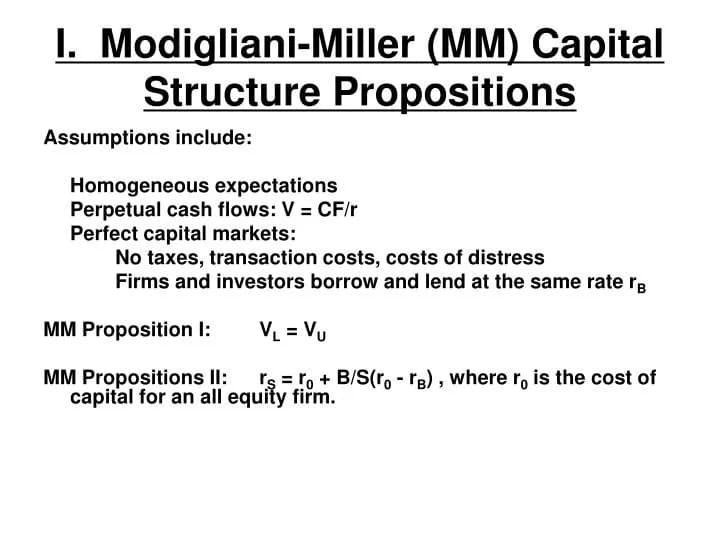

Corporate finance is the management of a company’s funds in a way that maximizes the value of the company and the role of capital structure, dividend policy, and corporate governance in this objective is well acknowledged. Capital structure: Capital structure is the amount of debt and equity that a company uses to meet its capital needs. Optimal capital structure minimizes the cost of capital while maintaining some degree of flexibility. The advantages of debt include the tax advantages while the disadvantage includes the high financial risk that comes with debt. On the other hand, equity financing is stable but is expensive and results in dilution of ownership.

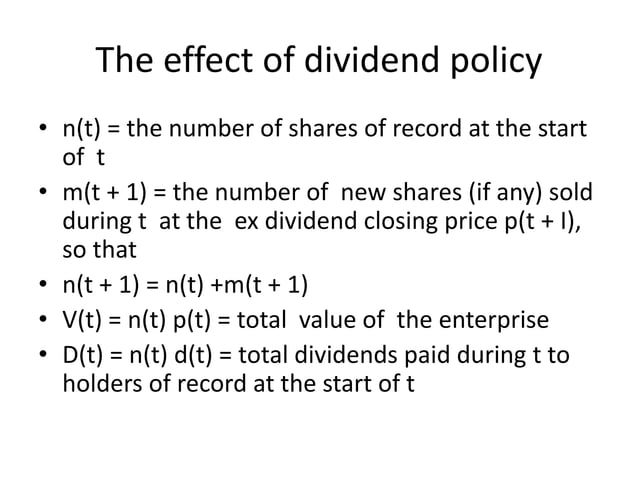

Dividend policy: Dividend policy addresses the issue of whether to pay dividends or to re-invest the earnings. A consistent dividend policy is attractive to investors who are looking for income and are reassured by the appearance of financial stability. But, for example, growing companies may decide to use the money for growth rather than pay dividends. This decision is dependent on the profitability, growth potential and expectations of the shareholders.

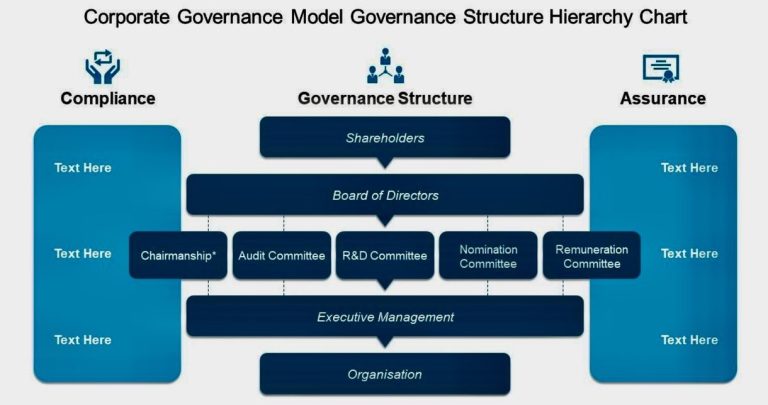

Corporate governance is the management of an organization in a way that guarantees that those in charge work to achieve the best results for the various stakeholders. Solid governance entails having an independent board, clear reporting, and ethical sailing, which minimizes agency costs, which are the mismatches between management and shareholder objectives, and increases accountability. Strong governance increases market confidence, which in turn improves a company’s ability to raise capital and its value.

Investment analysis is an approach that aims at realizing the highest returns with the least risks, with portfolio management, the risk-return trade-off, and asset pricing models being some of the core elements of this field. Portfolio Management - This process entails the selection and oversight of a number of different assets so as to attain pre-specified investment outcomes. It places much emphasis on diversification in order to avoid unsystematic risk by including assets that are not correlated. Active portfolio management tries to outperform the market through the selection of assets while passive management seeks to mirror the market through the use of index funds. Risk-Return Trade-Off - The risk-return trade off states the opportunity returns of an investment and the risks that are associated with it. High risk investments like equities are known to provide higher returns compared to low risk investments like government bonds. It is therefore the investor’s responsibility to ensure that their portfolio is in conformity to their risk tolerance and financial goals. Tools such as the efficient frontier of the MPT help in the identification of those portfolios that can provide the highest returns for a given level of risk. Asset Pricing Models – These are tools that are used to value assets and determine the risk premium. The Capital Asset Pricing Model (CAPM) is a significant model that relates expected returns to systematic risk, which is measured by beta. The APT expands this view to include several risk factors instead of a single risk. Other models that are more recent such as the Fama-French three factor model, bring in other factors such as size and value to a better understanding of the behavior of assets.

Behavioral Finance

Topic Focus: Psychological biases in financial decision-making.

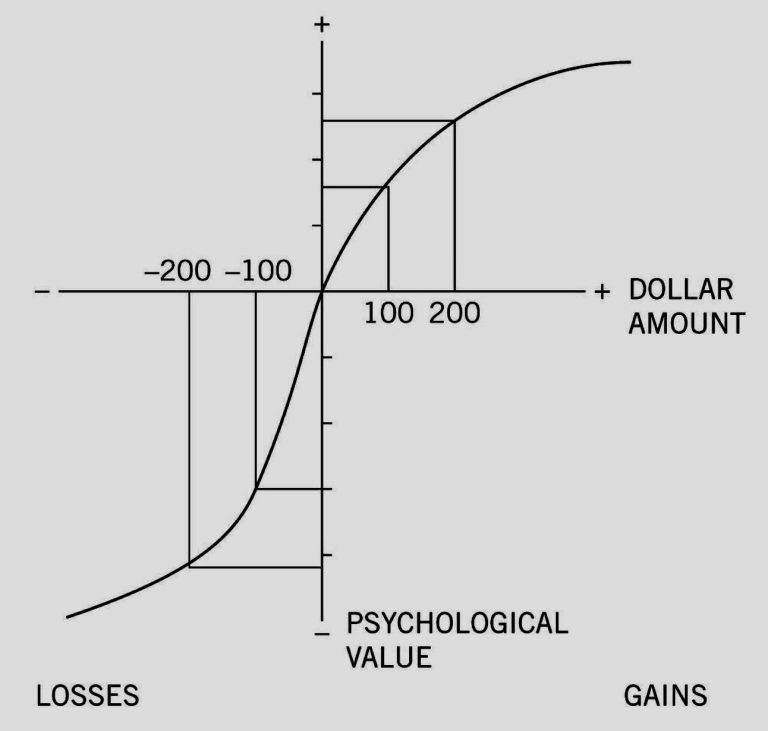

Behavioral finance studies the role of psychological factors in the field of finance, which results in irrational behavior of individuals. Such biases are caused by cognitive and emotional factors and affect almost all the participants in the market, including investors, consumers, and financial experts. Consequently, the effectiveness of the decisions made is usually not the best.

The most widespread bias is overconfidence, which means that people tend to think they know more or can do better than they actually can, which results in increased trading or high-risk investments. The confirmation bias tells the story of people looking for information that supports their point of view and not looking at the opposite side, which is detrimental to financial decisions.

Anchoring bias appears when people set their reference values based on the first available information, for example, the price of a stock, and use this reference to value other assets. The same is true for the herding hypothesis, which postulates that people tend to follow the crowd, e.g., in investing, which results in price bubbles or crashes as investors act based on emotion rather than reason. The present bias explains the preference for instant rewards as opposed to future gains, which can hinder optimal saving or retirement planning.

These biases are the emotional and cognitive prejudices that are inherent in the decision making process in finance. It is crucial to understand these tendencies for those who are seeking to improve their decisions. According to the behavioral finance theory, it is also possible to use such measures as diversification, as well as the advice of professionals in order to reduce the impact of these biases.

International finance focuses on the financial relationships between countries and includes aspects such as exchange rates, foreign investments, and global monetary systems. Exchange rates are very important because they fix the value of one currency against the other and, in turn, affect trade, investments, and economic plans. For instance, floating rates rise or fall on market forces while fixed rates are more comfortable but demand government supervision. Foreign investments are vital in the growth of the global economy as well as that of the member countries of the global economy. This category includes Foreign Direct Investment (FDI), where investors establish physical facilities or take over ownership interests in a foreign country, and Foreign Portfolio Investment (FPI), which is the acquisition of foreign shares or bonds. FDIs are usually more favorable to long-term economic development because they create employment and bring in technology.

Reference: Krugman, P., & Obstfeld, M. (2003). "International Economics: Theory and Policy." Pearson Education.

Financial risk management covers the activities that are involved in identifying, assessing and controlling the different types of risks that are likely to affect an organization’s financial status. The overall objective is to minimise losses and enhance sustainability by addressing the uncertainties that are associated with the financial functions.

The first step is identification which requires organizations to determine the different types of financial risk. Some of these sources may include market risks, credit risks, liquidity risks and operational risks. Based on this, effective identification is based on historical data analysis, industry observations and the use of risk management tools.

The assessment phase involves identifying the likelihood of occurrence and the possible impacts of the risks that have been recognized. This stage often employs quantitative tools such as VaR or scenario planning to determine the financial impact of different states. A correct assessment is essential for the purpose of determining which risks require immediate attention.

Mitigation seeks to reduce financial risks through preventive or corrective measures. Some of the measures that can be employed include; diversification, the use of hedging tools such as futures and options, setting of credit limits, and maintaining sufficient liquid assets. Also, the implementation of sound internal controls systems and external audits increase the ability of an organization to manage risks effectively.

Risk management is therefore not a one off activity but a process that is integrated into the overall plans of a company. Through these efforts of managing the financial risks, it is possible for the businesses to protect their assets, meet the requirements of the investors and be able to navigate through changes in the market, which in turn guarantees the organization’s sustainability in a volatile economic environment.

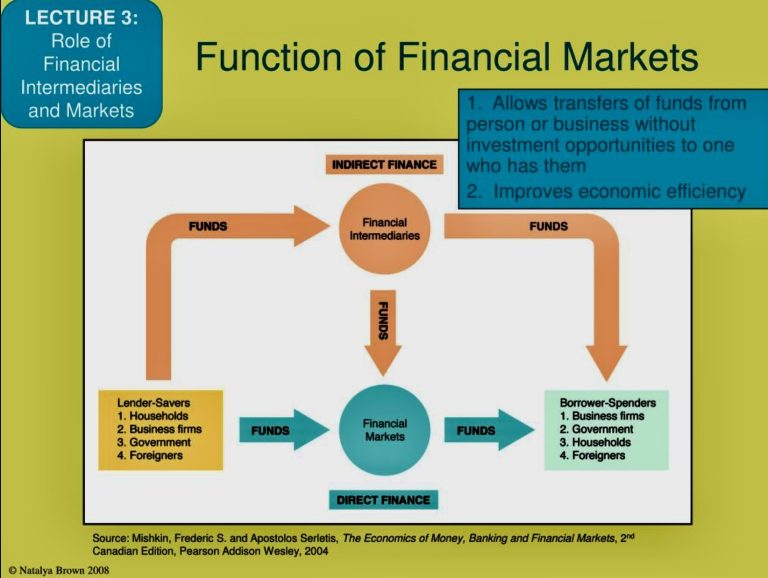

Topic Focus: The role and functioning of financial markets and intermediaries.

Financial markets and intermediaries are an important part of the overall economy because they bring about the channeling of funds from the saving sector to the borrowing sector. Financial markets are market for financial instruments such as stocks, bonds and derivatives. These markets are divided into Money markets which deal with short-term financial instruments like Treasury bills and Capital markets which are markets for long-term financial instruments like stocks and bonds. They are also important in the determination of prices, the provision of liquidity and risk transfer, all of which are important in supporting growth and stability of the economy.

Financial intermediaries include banks, insurance companies and mutual funds which act as go between for surplus and deficit units in the economy. They collect money from the public and re-allocate it to productive sectors of the economy through the provision of loans to firms, governments or individuals. Through risk diversification, liquidity provision and asset management, intermediaries enhance the effectiveness of the financial system.

Financial markets and intermediaries are therefore mutually dependent to sustain market efficiency and economic stability. For example, banks lend money and stock markets provide a means through which companies raise capital through the sale of shares.

Time Value of Money (TVM)- TVM is a basic financial principle that explains the price of money over a period of time. It highlights the fact that a dollar today is more valuable than a dollar at a future date because the dollar today can earn interest. Key components of TVM are Present Value, Future Value, and Discounting Cash Flows.

Present Value (PV)- Present Value is the amount that will grow to a future sum of money, at a given discount rate. It solves the problem, “How much is a future amount worth, today?” PV is useful for determining whether or not future cash flows are sufficient to justify an investment for investors and businesses.

Future Value (FV)- Future Value (FV) is the calculated value of a principal after a certain period of time, including the interest or returns. It reveals how the money is gained through compound interest, where interest can earn interest. FV is important in finance for example in setting financial goals such as saving for retirement or wealth creation.

Discounting Cash Flows (DCF)- The DCF method is a way of calculating the value of future cash flows by converting them to their worth in the present time. This technique incorporates the concept of the time value of money and risk and is used in almost all investment decisions and valuation models. The discount rate embodies the opportunity cost, inflation, and investment risk.

Public finance is the study of governments’ revenue and spending and their impact on the economy. Three key elements are central to public finance: They are government expenditure, taxation, and fiscal policy.

Government expenditure includes all the spending activities of governments to provide public goods and services such as education, health, infrastructure, and defense. It is necessary for improving economic growth, income distribution and the well being of citizens. Taxation is the main source of government funding. They collect taxes from individuals, businesses, and other public and private entities to raise the funds needed to pay for the government’s functions and investments. Equity, efficiency and revenue are the objectives to be achieved through tax policy. Progressive tax systems intended to equalize income are those that seek to have higher income earners pay more, while regressive taxes can affect lower income people more harshly.

Fiscal policy is the use of government spending and revenue collection to affect economic outcomes. Expansional fiscal policy, which comprises higher government spending or lower taxes, is used to boost the economy when the overall economy is in doldrums.

The Efficient Market Hypothesis (EMH), which was proposed by Eugene Fama in the 1960s, states that the market reflects all the information that is available, which makes it difficult for investors to earn above-average returns on a consistent basis. Fama classified EMH into three categories; weak form, which goes further to state that past price data is not useful in predicting future prices, semi-strong form which states that all the public information is already reflected in the prices and the strong form which holds that even insider information is already incorporated in the prices.

In view of EMH, active management is mostly inefficient because price changes are Brownian motion and therefore not predictable, tending to support passive management, such as indexing. However, the counterargument is that there is evidence of inefficiency through behavioral biases, market anomalies, and events like bubbles. Nonetheless, the EMH is still a critical theory for the analysis of market efficiency and the difficulty of realizing abnormal returns

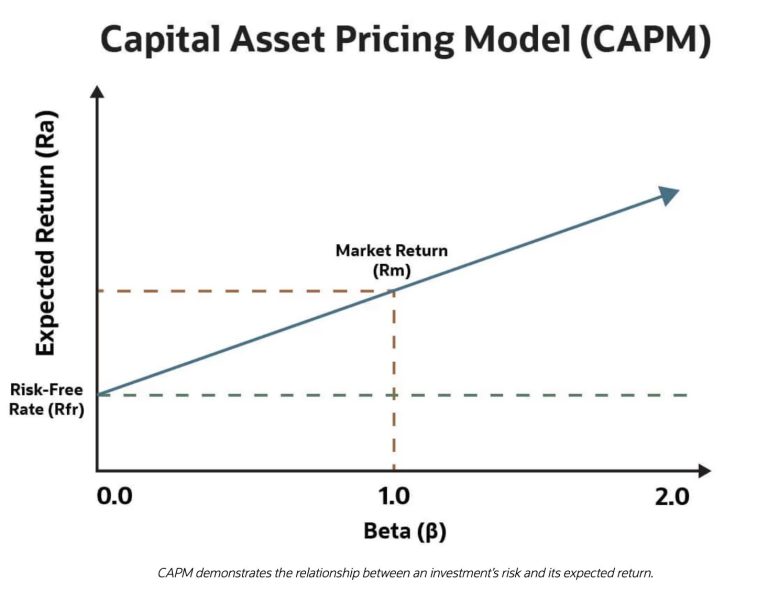

Capital Asset Pricing Model (CAPM)

Topic Focus: Relationship between risk and expected return

The Capital Asset Pricing Model (CAPM) is a theory that explains the relationship between the risk of a asset and the expected return on that asset. The theory states that the expected return of an asset can be explained by the risk free rate, the market risk or beta of the asset and the expected market return.

The formula is: E(Ri)=Rf+βi(E(Rm)−Rf)

Where:

• E(Ri) is the expected return of the asset,

• Rf is the risk free rate,

• βi is the asset’s beta,

• E(Rm) is the expected return of the market.

From the CAPM theory, higher risk that is beta requires a higher expected return to compensate for the higher risk. This model assists investors in making decisions on risk and return in investment.

Reference: Sharpe, W. F. (1964). "Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk." The Journal of Finance.

©Copyright. All rights reserved.

Wir benötigen Ihre Zustimmung zum Laden der Übersetzungen

Wir nutzen einen Drittanbieter-Service, um den Inhalt der Website zu übersetzen, der möglicherweise Daten über Ihre Aktivitäten sammelt. Bitte überprüfen Sie die Details in der Datenschutzerklärung und akzeptieren Sie den Dienst, um die Übersetzungen zu sehen.